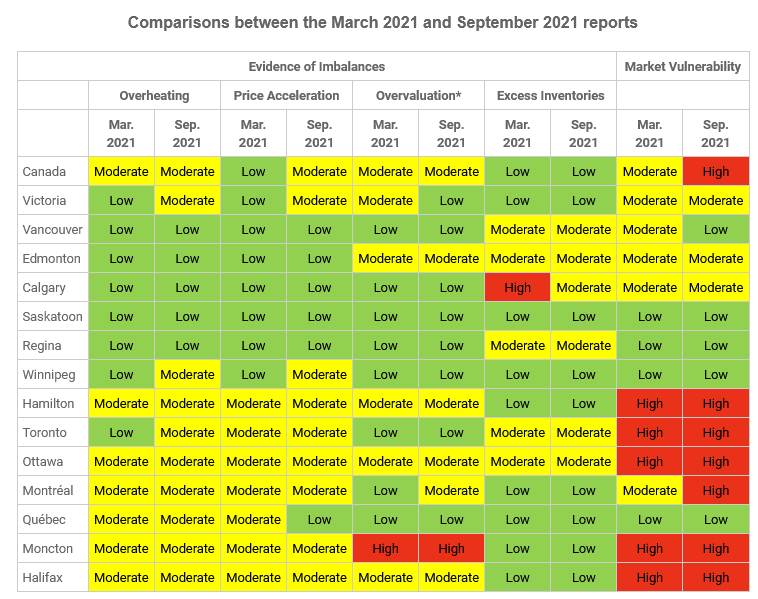

A few possible trends and risks to keep in mind

From rising inflation and falling consumer confidence to changing real estate preferences, Canada’s mortgage market impacts from multiple fronts.

Ben Rabidoux, a real estate analyst and founder of Edge Realty Analytics, recently participated in a webinar hosted by Mortgage Professionals Canada where he outlined some of the key trends that could impact mortgage rates.

Below is a summary of part of that discussion.

An “inflation scare” is coming

Inflation is running hot right now, with the latest reading from July at 3.7%, according to data released by Statistics Canada, well above the Bank of Canada’s (BoC) target of 2%.

Despite the Bank’s insistence that inflation pressures should prove “transitory” and dissipate as supply chains ease up, Rabidoux believes an “inflation scare is coming.”

That’s partially based on a survey by the Canadian Federation of Independent Business, which measures price expectations among Canadian businesses. The percentage of businesses anticipating price increases of more than 5% this year has spiked to nearly 45%, up from 24% at the start of the year.

“We know that businesses are seeing a lot of price pressure. That’s going to translate into higher inflation and I have a suspicion it’s going to end up being a little stickier than central banks will have us believe,” Rabidoux said.

If that comes to pass and inflation remains high, markets would likely see a rise in the 5-year bond yield, which is the leading indicator for 5-year fixed mortgage rates.

“If people get nervous that inflation’s going to stick around, you could see this rate tick up, and that would be bad news for fixed-rate mortgages,” Rabidoux added.

Potential reversal of the “flight to the suburbs”

Over the course of the pandemic, there’s been a flight of homebuyers out of the cities looking for single-detached homes with more space and privacy.

As a result, places like Bancroft, North Bay, have seen annual home-price appreciations of more than 64% and 48%, respectively.

“A lot of these areas benefited from this dynamic from the pandemic where people wanted more green space and lower density. They wanted single-family homes and couldn’t get it in the city, so by and large they started to push out,” Rabidoux said. “They also wanted recreational properties, which I think is a more important dynamic. And so you’re seeing a lot of these recreational property markets boom.”

But Rabidoux points to signs of that trend starting to reverse. The latest housing reports are showing declines in the detached market, particularly in the 905 area code, while condo demand is rising again in the 416.

“This suggests to me that we’re starting to see the early signs that this migration out of the big cities and into the suburbs is starting to reverse,” Rabidoux said. “I would be a little bit concerned that as we begin to open back up, that we might start to see a bit of an unwinding.”

That goes especially for the more “illiquid” recreational property markets in cottage country, where there are now signs of a softening in prices.

But as Rabidoux noted, “After places run up 60% year-over-year, it wouldn’t be shocking to see them pull back 10 or 15% from those highs.”

Waning in consumer confidence

Now in the midst of a fourth wave of Covid-19, consumer confidence has marked the steepest decline since the early days of the pandemic, according to the weekly consumer confidence index published by Nanos.

While confidence remains high, “we’ve seen a pretty significant softening in recent weeks,” Rabidoux noted. “This is something to watch, because the economy is ultimately a confidence game.”

He added that if the fourth “Delta” wave of the pandemic proves significant, it “could matter a lot for the economy and it could matter a lot for housing.”

Nanos also publishes a sub-index to measure how people perceive real estate to be performing, which has also seen a steady drop-off in recent weeks.

“This is maybe an early warning sign that people’s sentiment on real estate is starting to get a little bit soft,” Rabidoux said. “And that could translate into some soft home sales later this year and early next year. But a lot, I think, will depend on how this virus plays out.”

End of government income support measures

Now more than a year and a half into the pandemic, there are still 1.7 million Canadians on wage subsidy programs, which are scheduled to expire on October 23.

“That’s a huge number,” Rabidoux said, noting that during the financial crisis of 2008, there were 800,000 on employment insurance. “We’re at twice as many people still on government support compared to the height of the financial crisis.”

At the same time, the share of businesses reporting a shortage of workers is at a record high. Rabidoux notes that while the situation isn’t a huge deal at the moment, “we don’t know how this is going to play out.”

Housing affordability a key election issue

All of the major political parties have promised to make housing more affordable as part of their election platforms.

And for good reason, as there is currently a massive cohort of prime homebuying people in Canada, Rabidoux notes.

The most common age to purchase a home is now between 28 and 37. And with millennials now outnumbering boomers, housing affordability is an increasingly important election issue.

“Canadian politicians have to cater to this huge demographic of potential homebuyers,” Rabidoux said.

But on the flip side, housing now represents the overwhelming majority of the Canadian economy, accounting for two thirds of GDP since the bottom of last year’s recession, and over 50% over the past four years.

“We have a record share of our economy in Canada that’s driven by housing, so the government is going to have to tread really lightly here,” Rabidoux added. “As much as politicians want to make housing affordable, they want to be careful not to upend the economy in the process.”

This is why he believes most policies will be focused on incentivizing new housing supply.

Potential new regulations on the way

Mortgage debt has been growing at a record pace over the past year, and if that continues, Rabidoux suspects new mortgage regulations could come down the pipeline later this year or in early 2022.

He noted that regulators have been dropping hints and often emulate policies that have already been tested in other markets. He pointed to New Zealand, which faces a similar housing market characterized by supply constraints and high demand. The government there just announced a tightening of underwriting practices for secondary properties, which now require a higher down payment.

“I think you could see OSFI (the Office of the Superintendent of Financial Institutions) start to follow suit,” Rabidoux said. “It wouldn’t surprise me if we start to see higher down payment requirements for secondary properties or some form of restricting eligible down payment, so they might say you can’t borrow from a HELOC, you can’t finance an existing property to buy a secondary property, whether a recreational home or an investment property.”

Higher debt-to-income limits could also be considered, he added.

Wealth inequality a growing issue in Canada

In 2021, renters saw their household net worth increase by $8,000 over the first three months of the year, whereas homeowners saw a $73,000 increase.

“That’s an enormous inequality gap, and it’s driven by the dollar increase in house value in Canada,” Rabidoux said. Over the past year, homeowners have seen their values increase on average over $133,000.

“This is a topic of extreme importance to this government and I think the longer this dynamic goes on, it’s asking for some kind of radical intervention.”

While Rabidoux isn’t certain what that response might be, he said he would be “shocked” to see a capital gains tax on primary residences, except perhaps on the ultra-luxury market of houses valued over $5 million, for example.

Published by Steve Huebl